If you're thinking about buying a home, you've probably wondered what credit score you'll need to qualify. The short answer is that the higher your credit score, the better your chances of being approved. The longer answer is that it depends on many other factors as well.

Let's look at the minimum credit score required to buy a home for each loan type to discover what you can afford.

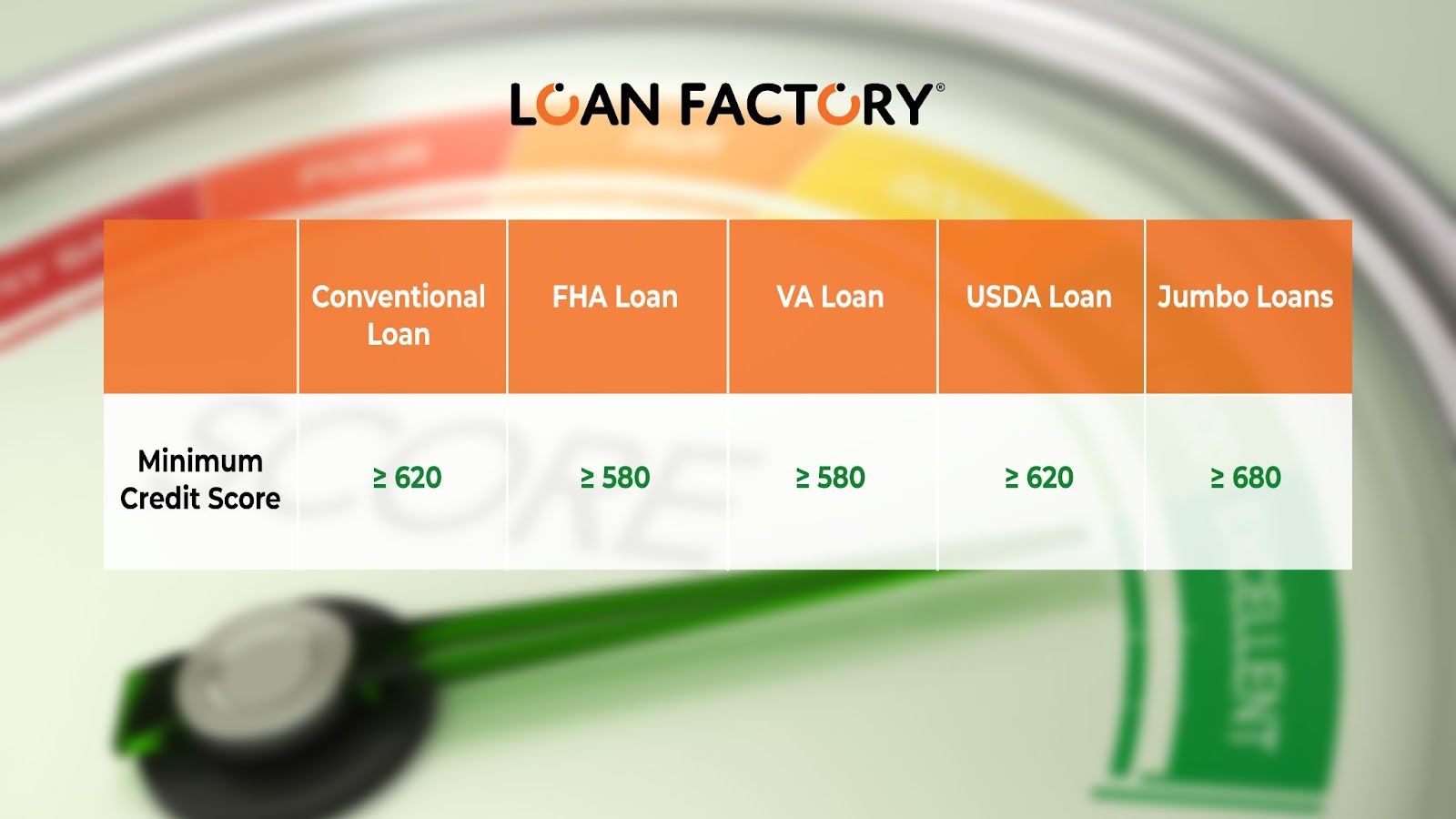

What Credit Score Do You Need to Buy a House?

Each loan program has its own credit requirements. On average, here’s what you can expect, although some situations may differ slightly.

Conventional Loan: 620 Credit Score

Conventional loans are traditional mortgage loans. The minimum credit score to buy a house or refinance with a conventional loan is 620. You can secure conventional loans at most mortgage lenders and brokers, and some credit unions too.

You’ll get a lower interest rate if you have a higher credit score with conventional loans, and if you put 20% or more down on the home, you won’t have to pay Private Mortgage Insurance.

FHA Loan: 580 Credit Score

FHA loans are a bit more lenient when it comes to the credit score required for a mortgage. You can get by with a credit score as low as 580 and a lower debt-to-income ratio and down payment.

VA Loan: 580 Credit Score

VA loans, which are backed by the Department of Veterans Affairs, don’t have a minimum credit score requirement. However, most lenders require a 580 minimum credit score to buy a house with VA financing.

This program is exclusive to military veterans and offers the most flexible restrictions, including no down payment and no specific debt-to-income ratio. As long as borrowers have enough disposable income to meet their family’s needs, they might be eligible for a VA loan.

USDA Loan: 620 Score

USDA loans are for low-income families that don’t qualify for any other financing program. The USDA guarantees loans to buy homes in less populated areas. Borrowers don’t need a down payment and the USDA requires a 620-credit score to buy a house, but you must prove your family is in need, which means your total household income cannot exceed 115% of the area median income (AMI).

Jumbo Loans: 680 Credit Score

Jumbo loans have the highest credit score requirements because they carry the highest risk. They offer loan amounts higher than the traditional $647,200 limit set by conventional and government-backed loans.

To make up for this risk, jumbo loan lenders require credit scores as high as 700 and down payments between 10 – 30%. These loans aren’t government-backed, so lenders take a risk when they lend the funds. A higher credit score reduces their risk of default.

How To Raise Your Credit Score

If you don’t have the minimum credit score for a mortgage, there are ways to improve your score. This won't happen overnight, and it will take some time on your end, but with some effort, you can increase both your credit score and your chances of getting approved.

Check your Credit

The first step is to check your credit report and determine what's affecting your credit score. All consumers get free access to their credit score here.

You can pull one credit bureau or all three. The key is to look over every tradeline, make sure it’s accurate, and that there isn’t any negative information. If you have late payments, you use too much of your available credit, or you apply for credit too often, you may want to change your habits to increase your score.

A big part of checking your credit is also checking for inaccuracies. Mistakes happen, but they can hurt your credit score. If you notice information on your credit report that isn’t accurate, despite it with the reporting credit bureau to get it corrected and to improve your score.

Good Habits That Can Help You Increase Your Credit Score

Every borrower has a different reason for his/her low credit score, but if you need a higher credit score to buy a house, here are some ways to achieve it.

- Pay your bills on time – Pay your bills on or before the due date. If you miss the due date, get caught up as quickly as possible, avoiding any 30-day late payments on your credit report. Your payment history makes up the largest part of your credit score, so this is crucial.

- Keep your credit utilization low – Your credit utilization is the comparison of your total outstanding debt to your credit line. Keep your balance at no more than 30% of your credit line to improve your credit score.

- Avoid applying for new credit – If you’re thinking about buying a house in the next year, avoid applying for new credit. Any new credit inquiries lower your credit score by a few points, which can add up.

- Keep old accounts open – Your credit age is a big part of your credit score too. The older your accounts are the better it is for your credit score. Try keeping as many old accounts open as possible to have a higher average credit age.

Keep in mind that any of these changes won’t affect your credit score right away. It could take 6 months to a year to see a difference, but consistency pays off.

Final Thoughts

You need a good credit score to buy a house, but it doesn’t have to be perfect. There are loan programs that will work with just about any credit score. The key is to improve your credit score as much as possible, so you get the best rates and terms on your next mortgage loan.